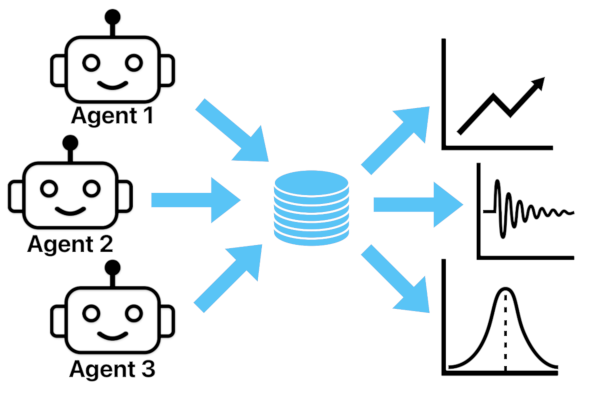

Agent-Based Market Simulation

A Python-based agent-based simulation (ABM) that models the dynamics of a financial market by simulating interactions between autonomous trading agents. Each agent follows distinct behavioral rules and submits limit or market orders to a fully custom-built limit order book (LOB) engine implemented from scratch.

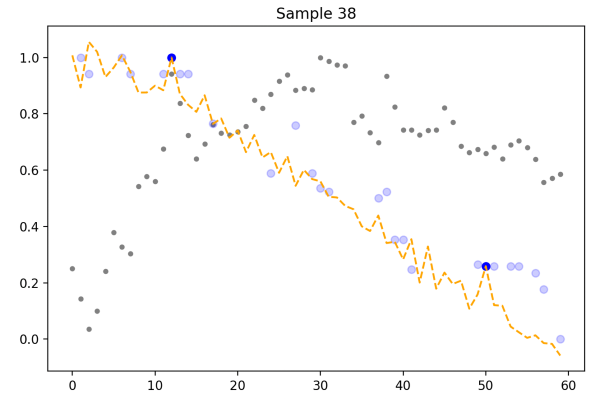

The platform serves as an experimental environment for studying market microstructure, developing and testing trading strategies, and analyzing emergent phenomena such as price volatility, bid-ask spreads, and liquidity dynamics. By simulating various agent types — such as market makers, noise traders, and arbitrageurs — this tool enables exploration of how individual behavior aggregates into collective market outcomes.